How to Create Your Debt Snowball & Get It Rolling

Sep 20, 2019

So many people have been able to pull themselves up and out of the hole of debt using the Debt Snowball. It’s a very simple and useful technique that when used properly and with diligence can make a huge impact on debt. It pays your debt off the fastest and with the greatest amount of savings over nearly every other method. This article explains and gives you the simple steps and rules to create your own Debt Snowball. I’m going to use the word “card” or “debt” interchangeably here because most people use snowballs to pay off credit cards. However, you can put any type of debt into your snowball; a mortgage on a house, a car payment, or even medical bills. It works for all types of debt.

What is a Debt Snowball?

A Debt Snowball describes a technique of taking one lump sum of money each month and applying it towards several debts, like credit cards, in such a way that seems small at first, but its impact grows over time. As each debt is paid off, more and more can be applied towards the next, like a snowball rolling down a hill and gaining size and momentum.

How Does It Save Money?

Because you are paying off the debt with the largest amount of interest first, it saves you money, sometimes thousands of dollars in interest charges over time. There are those who like to pay off the debts by amounts, smaller amounts first, giving people reason to celebrate sooner, small wins that keep them motivated. However, a true Debt Snowball focuses on saving interest payments and saving you money, which I believe is a much bigger reason to celebrate. It also takes the least amount of time because it saves you the most amount of money. Depending on your debt, you may not be able to celebrate right away, but you’ll be completely out of debt faster and will have saved the most amount of money using this technique.

What Do I Do First?

Before you even begin planning your Debt Snowball, you should do a couple of things. First, you should call your credit card companies and ask them to lower your interest rate. This will save you interest payments and that means more money in your pocket. Even if they won’t, it doesn’t hurt to ask.

Next, ask each credit card company to raise your spending limit. Only do this if you are a smart and disciplined person because otherwise you’ll just go on a spending spree and rack up even more debt. However, if it’s possible, raising your limit will do two things for you; it will increase your debt to income ratio, which could potentially raise your credit score, and it may create room for you to transfer balances from higher interest rate cards to lower interest rate cards, saving you money. If you have room on these lower interest cards, ask them to mail you a check to use to transfer the balances of higher rate cards to their card.

Warning: Don’t do this if you can’t be a responsible spender. The ONLY way to get out of debt is to spend less than you are making. If you are a shopaholic, raising your credit line will only tempt you to go further into debt. If you cannot control your spending, I suggest therapy. I’m not joking. Overspenders Anonymous and Debtors Anonymous are two organizations I recommend. They will support and educate you through the process of getting out of debt and help you get your spending under control because that is crucial. Again, the only way to get out of debt is to spend less than you are making.

What Else Should I Do?

Here are some rules for getting out of debt you have to be willing to follow if this is going to work. A hardcore commitment to the plan is absolutely necessary for it to work. You can’t be neutral. You have to be committed. Your mindset has to be, “I refuse to be in debt any longer. I control my money. It does not control me.” Once you can commit, follow these five rules.

1. Take full responsibility for your money and how you spend every penny.

2. Never spend more than you make.

3. Create a budget and stick to the budget.

4. Be disciplined.

5. Be consistent.

Now You’ve Got the Rules, Here are the Steps to Creating Your Debt Snowball

I’m going to create examples in each step using red to help you follow along.

Step One

In your monthly budget, gather all your information about your credit cards and any other debt you want to add into your snowball.

Find out the exact balance, the interest rate you’re being charged, the minimum payment due, and the due date of each debt you are paying off.

Step Two

Arrange your debt in order of interest rates, highest to lowest.

Step Three (You can skip this step if it’s too complicated or there are fees involved)

Remember, you’ve already called to get the interest rates lowered and the credit limits raised. A Debt Snowball is created in order to save you money in interest payments and pay off your debts the fastest way possible. There are other ways that get technical keeping credit scores in mind, but we are focusing on eliminating debt fast and paying the least in interest charges along the way.

So, with that in mind, if there is any room on your lower interest cards, you want to transfer whatever you can from the highest interest cards.

For our example: Credit Card 1 has a $2500 limit. Credit Card 2 has $1000 limit. Credit Card 3 has a $4500 limit.

We will take a check from Card 2 and pay $245 towards Card 3, your highest interest rate card. Paying off the highest interest card first saves you the most money. You can then do the same on Card 1 by paying $150 towards Card 3. Make certain you aren’t paying any fees for these checks that would eliminate the interest you would save transferring in the first place. If there are fees, then just leave the balance where they are. I’ve adjusted the balances below.

Step Four

Determine exactly how much money you can afford to pay towards these debts combined. The more you can put towards the snowball each month, the better. I would even give things up, like going out, in order to pay off my debts faster. The amount is up to you, but it should be the most that you can afford without making you struggle.

I have $500 in my budget each month to apply towards all four of these loans.

Note: You must be able to apply more money towards paying off those debts than the total of the minimum payments of all those debts combined. In the example, the total of the minimum payments adds up to $180. If I don’t have more than $180 each month to put towards those debts, I’m going to have to use another method. If this is the case, I suggest you speak with a credit counselor.

Step Five

Take the amount you are applying towards your debt each month and subtract the total of the minimum payments. This amount will be added to the minimum payment of your highest interest debt until it is paid in full.

$500 (my determined budget) - $180 (total of my minimum payments) = $320 (extra towards Card 3)

I will be paying the minimum amount due on every debt except Card 3, which is my highest interest debt. To that payment, I will add an additional $320 to the minimum payment until it is paid in full.

Step Six

Set up automatic payments through your bank or the credit card companies on each of your snowball debts, then just leave them alone to do their work. Just make sure you always have money in your account a day or two before the money is to be withdrawn.

With credit cards, it is best to set up an automatic minimum payment on the credit card’s website (or you can call them to set it up by phone). The reason is that credit cards love fees, it’s how they make the majority of their money. A trick they like to play is changing due dates by a day or two each month or changing your minimum payment amount without you noticing. Next thing you know, you have a late payment fee that dings your credit and that’s not good. Setting up with each card’s website avoids any such mishaps. You’ll see the minimum payment and the date when you set it up. If anything changes, they’ll make the adjustment and change the payment amount because you set it to “minimum payment.”

Paying through your own bank’s online bill pay is safer to do on everything else. You never, ever want a hospital or collection agency to have your bank or credit card information. Those little tricksters have been known to pull money without authorization, so don’t take that chance. Major credit card companies wouldn’t risk the lawsuits, so using their sites work well.

Step Seven

Determine how long it will be until your highest interest card is paid off. You can use any credit card calculator to do so, or just use your best guess by watching your account’s statement closely. Here’s a link to a Payoff Calculator you can use. Just ignore any ads that come up when you’re using any such tool online. This one gives you a table that shows your payments being applied as well as the last month’s payment amount, which is useful.

http://www.creditcards.com/calculators/payoff.php

Here’s what that table looks like:

I can see that in 12 months, Card 3 will be paid off. Woop! Woop!

Step Eight

When you’re in that final payment month for your highest interest card, it will be time to start the snowball rolling again. The final month can be odd because you might be splitting a payment. Just remember, when you roll the ball, you are only playing with your top two interest cards, the one that you’re about to pay off and the next highest interest card. This is how you’ll make that final payment because…

You’ve now paid off your first and highest interest credit card! Ta Da!

In our example, the final payment for Card 3 is 12 months later and the payoff amount will only be $171.04 instead of our usual $380. That means that I can apply the difference towards my next highest-interest card, in this case, Card 1.

Card 1’s balance at the end of 11 months is $2336.32 (using the calculator or just look at your statement’s balance). So instead of paying $45 (my minimum payment on that card), I’m going to pay $45 plus whatever is left over from my usual large payment to Card 3 ($380 - $171.04 = $208.98)

$45 + $208.98 = $253.98 becomes my payment for month 12.

In month 12, we will pay $171.04 to Card 3, paying off the card completely. We will pay $253.98 to our next highest-interest card, Card 1. Again, we only touch our two most expensive interest rate cards or debts. We leave the other debts alone.

The Next Month Begins a New Snowball Payment Plan

We’ve left all the other debts alone, keeping them at their same minimum monthly payment. Our highest interest debt was paid off last month (we’re still celebrating), so it’s time to roll that payment ball completely over to our next highest interest debt.

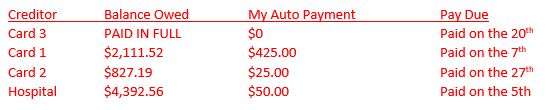

We will take the complete payment of what we were paying on the card that’s now paid off, the highest interest rate card (in our example, Card 3) and we are going to add that to our next highest interest card (in our example, Card 1).

$380 (Card 3’s old payment) + $45 (Card 1’s minimum payment = $425 (Card 1’s NEW payment)

That’s rolling the snowball. Now our bills look a bit different. Here’s our new payment schedule.

IMPORTANT: Set up the new autopay on your new highest interest card for the new amount. Then leave your Debt Snowball alone to do its magic.

Now it becomes like a wash, rinse, and repeat scenario. Each time you get to a month when a debt is about to be paid off, you just roll the old payment onto the next highest interest card. The new larger payment will begin paying each card down faster and faster. Let’s look at our examples.

In our example, because we were able to increase our payment to $425, we will have Card 1 paid off in only 6 months! Sweet, right?

So, 6 months later (or month 18 from the start), we will only have a balance of $68.83 on Card 1. We will pay off Card 1 and roll the extra $356.17 into Card 2’s payment, our next highest interest card. Card 2’s payment becomes $381.17 for that month. All other payments, in this case just the hospital, would remain unchanged.

What’s super-duper neat is that our balance on Card 2 is now only $367.43. That means we don’t even have to create a new Debt Snowball. We’ll have only one partial payment left on our final credit card and the rest can be applied to the hospital balance ($132.57 will go towards the hospital).

The next month, we can put the entire $500 towards the hospital debt, our only remaining debt. Our payments will look like this:

It would only take 6 more months to pay this debt off completely.

That’s how you do it! Now you don’t have to calculate the balances and do any work other than figuring out what the minimum payments are and how much to put towards your highest interest bill. Your statements will let you know when you’re close to your final payments. There are also calculators and debt programs out there you can use, but this is free and it works.

Is There Anything I Should Not Do?

Don’t add to your debt. If you are ever going to take control of your money, you have to control your spending. It really goes without saying. You can’t pay off credit cards if you are charging on them every month. If you say you need to, then you are living above your means. You are going to have to cut expenses somewhere and learn to live on less than what you make. Otherwise, you’re just digging that debt hole deeper and deeper each month.

Never decrease your debt reduction amount. This means when a debt is paid in full, your debt reduction amount doesn’t change. It stays the same. The money going towards that old debt doesn’t become extra spending money once a card is paid off: it rolls downhill like a snowball into a larger amount to be paid towards the next debt. It doesn’t decrease. It only increases in size. So, if you agreed to put $2,000 towards your debt per month, for instance, then you will continue to put $2,000 per month towards your debt each month until every single debt is paid off.

What Else?

Increase your payments towards your Debt Snowball whenever you are able. If you get a big check from a bonus or tax return, put that towards your highest interest debt instead of blowing it on something you can probably live without, at least until you are debt-free. Once you are debt-free, you will have that entire amount (in our example, $2000 per month) to put towards whatever it is you want; savings for retirement, an emergency fund, or maybe a newer car.

Most Importantly, Know Why You Want to be Debt Free

Debt-free living can literally extend your life! This is a medical fact. Being debt-free releases stress and stress can kill you. It is important, whenever you’re feeling the urge to purchase something, anything, to sit down with yourself or your significant other and go over the reasons why you want to be debt-free. Imagine the feeling of knowing that you don’t owe anyone anything. It’s a wonderful feeling. It’s freedom. I don’t owe anyone anything. Nothing ties me down. If I suddenly decided to move to another country, I could do it. If I want to change careers, I have money in the bank to do so. No one and nothing influences my decisions but me and my husband. We are in complete control because we are debt-free. I want that feeling for you! I want you to be free, too. Take control. You can do it. It’s not hard, but it does take self-control and discipline. You may slip, but I have faith you’ll put yourself right back on track. You’re smart and you deserve to live with the peace that comes from being debt-free.

Michelle R Russell

© The Prosperity Process, LLC

for BNB-Boss

Want to hire a Virtual Assistant but don't have a clue about how to get started...

We've created a program just for you inside our membership, VA Advantage. Not a member yet? We've got you covered, too. We've made this program available for "outsiders" for a limited time and for less than $20. Grab it now before it's too late!

Go and Grow...

If you want to become financially free, you need the right education. That’s why we created our Mini-Courses on investing in Short-Term Rentals. If you are serious about investing your time and money into an Airbnb (aka Short Term Rental), you need a system. Our courses are jammed packed with everything you need to know to create massive, passive income. Plus, they're affordable.

and take a look at July's BNB Budget Makeover Series inside our blogs...

This month, we give you loads of great ideas on using your orphan days to make inexpensive changes to your properties. Begin here, with Budget Room Makeovers: Weekend Projects for Under $1000.

Don't miss a beat!

New articles, blogs, podcast episodes, and courses delivered to your inbox.

We hate SPAM. We will never sell your information, for any reason.